By Sophia Lopez, Founder & Chief Researcher — Cryptophia Research | 11 April 2026

Conclusion

Ethereum’s network metrics are at or near all-time highs. Its token price is not. The instinct to read that as a bullish setup is understandable, but it misreads what the data actually shows. High activity and record stablecoin supply are evidence that Ethereum is a functioning settlement layer — not evidence that capital is rotating into ETH. Until that distinction resolves, the divergence is a reason for caution, not conviction.

The Mechanism

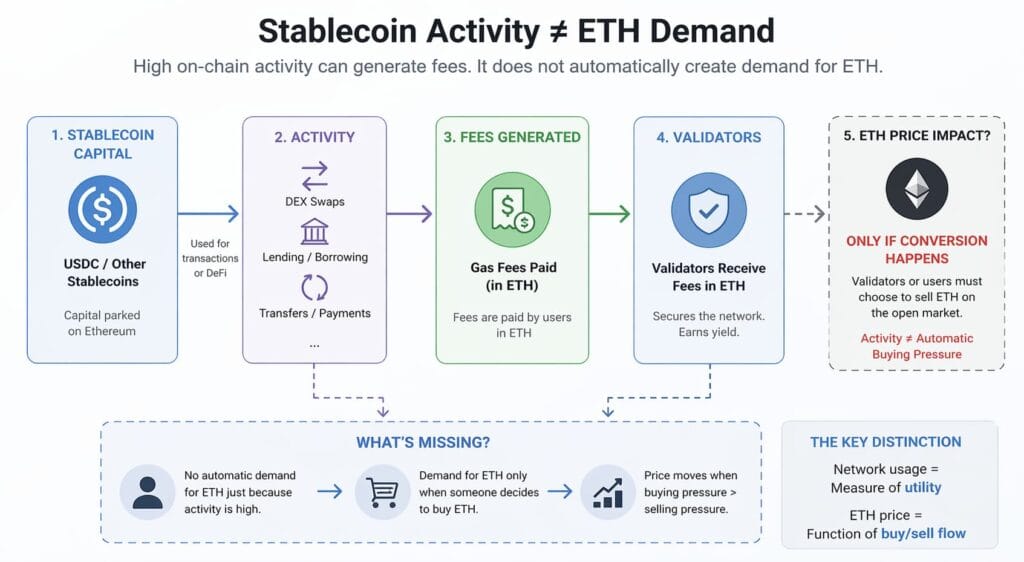

On-chain activity measures what is happening on the network. It does not measure demand for the network’s native asset.

These are different things, and conflating them is the central error in most ETH commentary right now.

A stablecoin sitting in a smart contract on Ethereum is using Ethereum’s blockspace. It is not waiting to become ETH. A DeFi transaction settled in USDC generates fees, contributes to transaction counts, and registers as “activity” — but none of that flow touches ETH as an asset unless a holder chooses to convert.

This distinction is structural, not temporary.

The Evidence That Matters

Three data points define the current setup:

1. Network activity is genuinely elevated. Ethereum’s 7-day average transaction count reached 1.3 million per day as of approximately April 9, matching the mid-February peak. Raw daily counts from YCharts confirm the trend: 2.566M on April 7, 2.423M on April 8, 2.370M on April 9. The network is being used.

Daily transaction count on the Ethereum network. Source: Glassnode

2. Stablecoin supply on Ethereum is at a record $180 billion. This is the most important data point in the brief — and the most misread. $180B in stablecoins sitting on Ethereum means deep, liquid capital is present on the network. It does not mean that capital intends to buy ETH. It is parked. It is available. It has not moved.

3. ETH price has not confirmed. Price traded between approximately $2,079 and $2,250 across the same window. That range, while not a collapse, shows no meaningful bid from the capital that is demonstrably present on-chain. If $180B in stablecoin liquidity and peak transaction activity were sufficient conditions for ETH appreciation, the price would reflect it. It does not.

Ethereum (ETH) Price Prediction. Source: InvestingHaven

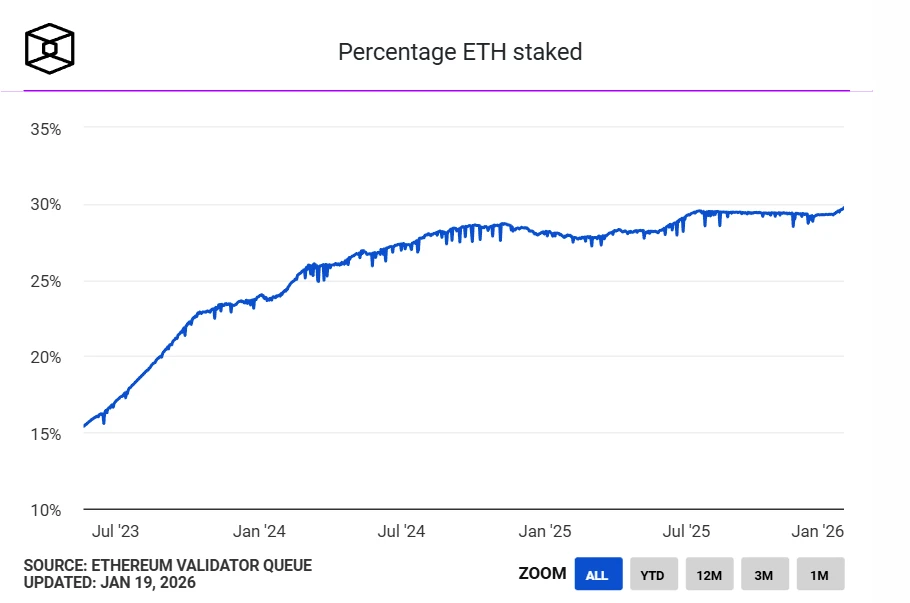

4. Staking is not a short-term price catalyst. Over 30% of ETH supply is now staked — approximately $85B in total value. This is structurally positive for supply reduction, but staking commitments are not short-cycle. Locked supply does not create near-term buying pressure; it removes near-term selling pressure. These are not equivalent.

ETH staking ratio. Source: Odaily

Separating Signal from Noise

The Glamsterdam upgrade — a protocol-level PBS implementation expected in H1 2026 — has not yet launched. It represents a pending change to validator economics, not a current catalyst. It should not be weighted in the present analysis.

Similarly, the broader ETF inflow data ($471M on April 6) pertains to Bitcoin, not Ethereum. Ethereum ETF flows have not been reported at comparable levels this week. Do not import Bitcoin’s institutional narrative into an ETH thesis without direct evidence.

The staking figure and transaction counts are real. They are just not doing the analytical work that much of the commentary assumes.

Market Structure Context

ETH’s price structure provides no additional support for a near-term bullish case. The $2,079–$2,250 range is narrow and directionless. There is no evidence of trend acceleration, and BTC’s own recovery this week — driven by geopolitical relief rather than crypto-native demand — has not pulled ETH decisively higher. In a risk-on rally that benefits BTC, ETH’s underperformance relative to its own on-chain strength is itself a signal.

Breadth is not constructive. A network running at full utilisation while its token lags the broader market recovery is not a setup that implies imminent price convergence.

Stance and Implications

The evidence supports the following judgment: Ethereum the network is performing well. Ethereum the asset is not currently benefiting from that performance.

For that to change, one of two things must happen:

- Stablecoin capital begins rotating into ETH (evidenced by stablecoin burn or redemption, rising ETH-denominated DeFi deposits, or direct ETH accumulation on-chain)

- A macro shift — easing liquidity conditions, a weaker USD, falling real yields — generates broad risk appetite that lifts ETH alongside other risk assets

Neither condition is currently in evidence. The divergence is real and has persisted. Until it resolves, the strong on-chain data should be read as a network health indicator, not a price entry signal.

State the uncertainty plainly: if macro conditions shift quickly, ETH could close this gap fast. The stablecoin capital is there. The rotation just has not started.

Cryptophia Research. Signal over noise.

Sources

- Coinfomania — “Ethereum Activity Hits All-Time High With 1.3M Transactions,” April 9, 2026

- MEXC — “Ethereum Stablecoin Supply Hits $180B ATH — Up 150% in 3 Years,” April 7, 2026

- Phemex — “Ethereum Stablecoin Supply Reaches $180 Billion,” April 6, 2026

- MEXC — “Ethereum Network Activity Hits All-Time High While ETH Price Diverges,” April 9, 2026

- Ethereum.org — “Ethereum Roadmap” (Glamsterdam upgrade details)

- BingX — “What Is the Ethereum Glamsterdam Upgrade,” April 5, 2026

- Investing.com — “Ethereum Staking at 30% of Supply Tightens Available Market Float,” March 17, 2026

- Fortune — Ethereum Price Data, April 7–9, 2026

- MEXC — “U.S. Bitcoin and Ethereum ETF Inflows Draw Focus After April 7 Report,” April 7, 2026

- CryptoQuant — Ethereum Daily Transaction Count, cited via Coinfomania and MEXC, April 7–9, 2026