The consensus for 2026 is remarkably tidy. Bitcoin hits new highs. The four-year cycle delivers. The Fed blinks, the dollar rolls over, and institutional capital — already positioned through spot ETFs — rides the wave. Grayscale published it. Analysts priced it. Half of crypto Twitter has already spent the gains.

I want to show you what the data actually says. Because the structural picture underneath that narrative looks nothing like accumulation. It looks like distribution into a story.

The Four-Year Cycle Is Not a Law of Physics

Let’s dispose of this quickly. The four-year cycle thesis is pattern-matching dressed up as analysis. It takes three data points — 2013, 2017, 2021 — draws a line, and calls it a framework. It doesn’t explain why those cycles happened. It doesn’t account for mechanism. It says nothing about what happens when the cohort driving the cycle decides the top is closer than the bottom.

Grayscale citing it as a price catalyst is not a signal. It’s marketing copy with a chart attached.

The actual question is not “are we in year two of a four-year cycle?” The actual question is: who is buying, who is selling, and what does the liquidity environment permit? When you ask that question, the picture sharpens fast — and not in the direction the consensus is pointing.

The Macro Floor Is Real. It’s Just Not a Launch Pad

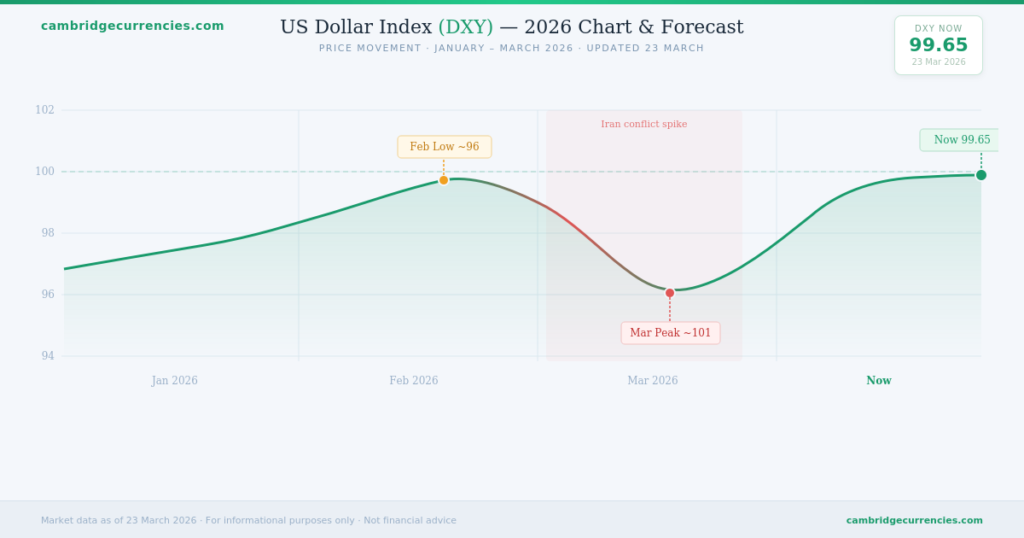

I’ll give the bulls this much: the macro backdrop has improved at the margin. DXY is down ~2.25% over the past 30 days, sitting at 98.10. The Fed’s balance sheet expanded by $18B in the week ending April 8. M2 growth is running at 4.4–4.5% year-over-year. These are not nothing. Dollar weakness and marginal balance sheet expansion are genuine tailwinds for risk assets — Bitcoin included.

But a tailwind is not a tide. Context matters.

The 10-year real yield is sitting at 1.96%. That number tells you the cost of capital is still meaningfully positive in inflation-adjusted terms. We are not in a zero-real-rate environment where cash burns and every asset floats. We are in a world where holding dollars still has a real return — which means capital doesn’t need to reach for risk. The macro environment has shifted from aggressively restrictive to mildly less restrictive. That’s a different call than “easing cycle is here, size up.”

The DXY decline is the most important variable to watch. If it persists and breaks through the 97 handle with conviction, the liquidity argument strengthens considerably. Right now, it’s a month-long drift, not a structural reversal. One month of dollar weakness after a two-year cycle high is a data point, not a thesis.

The macro floor is real. Use it to frame the downside, not to justify the upside.

DXY 2026 Chart. Source: cambridgecurrencies

The Chain Doesn’t Lie, and Right Now It’s Telling You Something Uncomfortable

This is where the consensus narrative falls apart.

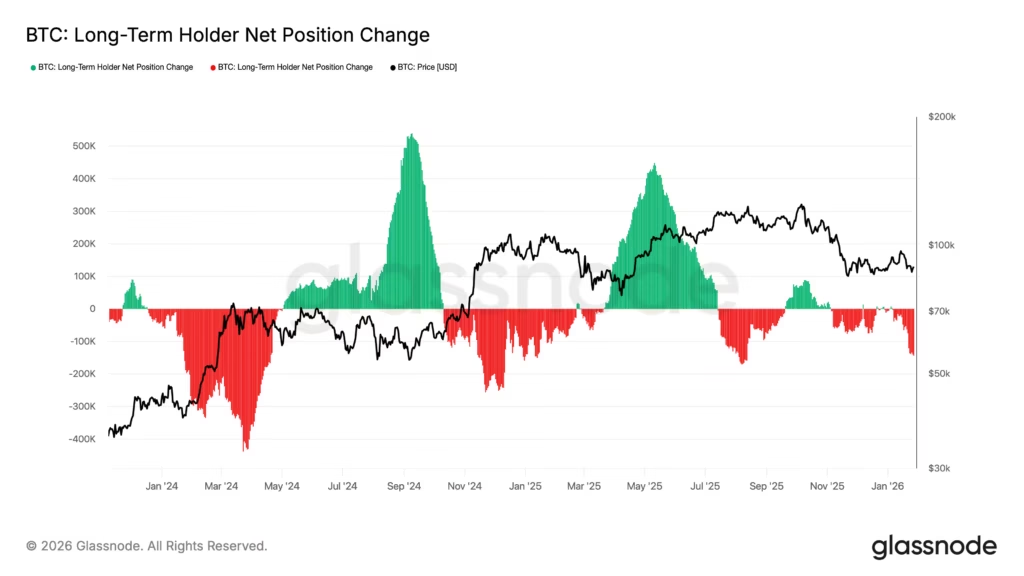

Long-term holders — the cohort defined by wallets holding Bitcoin for more than 155 days, typically the highest-conviction, lowest-cost-basis participants in the market — reduced their supply by ~116,400 BTC over the past 30 days. That’s not a rounding error. That is the most structurally meaningful on-chain signal available, and it is pointing the wrong direction for the bull case.

Long-Term Holder Net Position Change. Source: Glassnode

LTHs don’t sell because they’re scared. They sell because they think price is high enough to realize. When this cohort distributes at scale, the historical read is consistent: they’re offloading into narrative-driven demand, often retail, often late-cycle. The question isn’t whether 116k BTC is a lot in isolation. The question is who is absorbing it — and whether that buyer has staying power when the story softens.

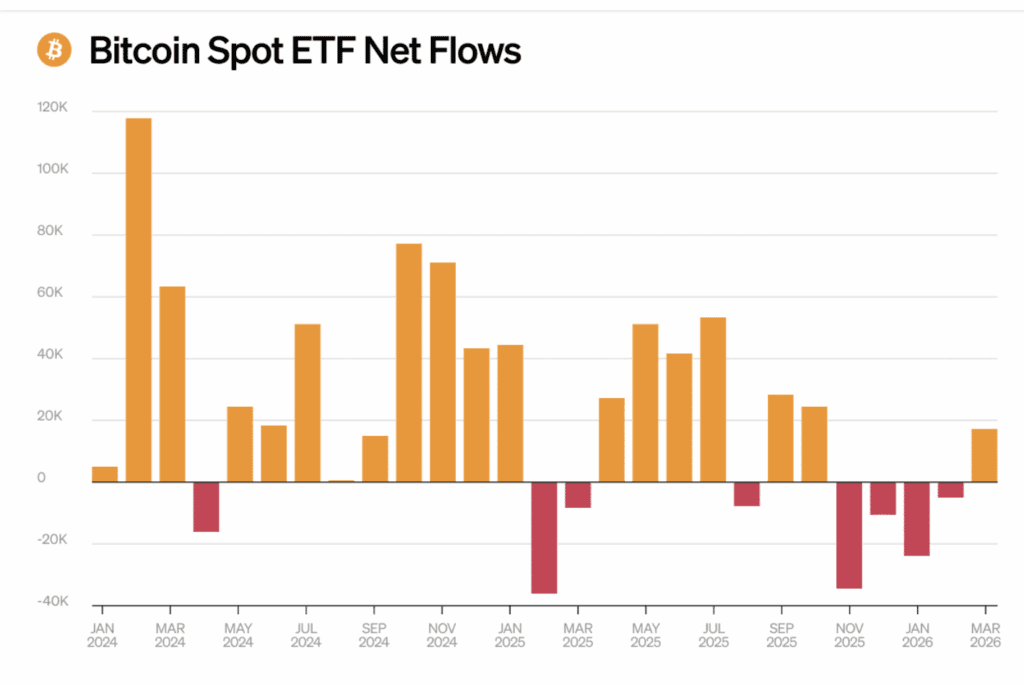

Now layer in the ETF flows. Over the past seven days (ending ~April 11), spot Bitcoin ETFs saw net inflows of $1.1B. BlackRock (IBIT) added $871M — but watch if this is rotation or pause. Fidelity shed $39M. BlackRock added $28.8M — the only institutional name still in net accumulation mode, and not by enough to offset the rest. Ethereum ETFs saw net outflows of $130M for the week, with BlackRock a net seller.

The “institutional bid” narrative depends on ETF inflows as its proof of concept. Right now, that proof isn’t showing up in the data. Net institutional flow across both major spot products is negative. That doesn’t mean the bid is gone permanently — but it means the people who were supposed to be the cycle’s structural buyers are, at best, pausing, and at worst, reducing.

One signal cuts the other way. USDC saw net minting of $253M in a recent 12-hour sample. Stablecoin creation at this rate usually means one of two things: capital staging ahead of a buy, or capital rotating defensively out of risk assets into dollar-denominated holdings. I don’t know which one this is yet. Neither does anyone else. What I do know is that $253M in stablecoin minting next to $60.5M in ETF outflows and 116k BTC of LTH distribution does not add up to a clean accumulation signal. It adds up to a market that is confused about where the next leg goes.

The exchange net flow for BTC in the past 24 hours was −$420k, meaning coins are still leaving exchanges on net. That’s a mild positive — it suggests some holders are moving to cold storage rather than staging for sale. But one day of exchange outflow is noise. The 30-day LTH trend is signal. I’m weighting accordingly.

Bitcoin Spot ETF Net Flows. Source: Markets Media

The Positions That Break First If the Story Softens

Miner outflows are elevated. I don’t have an exact dollar figure for the past seven days, but elevated miner selling in a post-halving environment against a backdrop of sideways price action is a structural pressure point. Miners operate on thin margins post-halving. They sell when they need to cover costs. They sell more when price doesn’t move in their favor. If the macro tailwind stalls, miner sell pressure doesn’t disappear — it accumulates.

The derivatives picture is cleaner. Funding rates are sitting at 0.0082% on an eight-hour average — positive, but barely. Perpetual traders are net long, not aggressively so. Open interest as a percentage of market cap is at 2.1%, which is relatively low by cycle standards. This cuts both ways. On the bullish read: not much speculative leverage in the system, so no imminent cascade risk. On the bearish read: there’s no trapped long to fuel a squeeze higher. The move up, if it comes, has to be driven by spot demand — and spot demand, per the ETF flows, is currently net negative.

The options skew is the tell I keep coming back to. The 30-day delta skew is at 12% put-call premium, indicating the derivatives market is paying up for downside protection. That’s not extreme fear — but it’s a market that is not positioned for euphoria. If the consensus was genuinely confident in a 2026 breakout, that number would be collapsing, not sitting at an elevated put premium.

The fragility lives here: LTH distribution feeds into exchange supply, miner selling adds more, ETF outflows reduce the institutional absorbing capacity, and a derivatives market that is paying for puts doesn’t have the positioning structure to run hard. A DXY reversal — dollar strengthens, real yields stay elevated — and that entire stack becomes a problem simultaneously.

The Scenario Nobody Is Pricing in the Cycle Deck

Here’s the ugly path. The dollar stabilizes. Real yields don’t budge — the Fed is not cutting into above-target inflation and a labor market that hasn’t broken. The macro tailwind that justified the early 2026 narrative fades. LTH distribution continues, now into a bid that’s thinning. ETF outflows pick up. Retail, who bought the cycle story, starts to notice price isn’t moving up despite the narrative. Miner selling doesn’t stop — it accelerates as margins compress.

The cascade mechanism isn’t leverage in this setup. It’s supply overhang meeting demand exhaustion. LTHs and early ETF holders offloading into late-cycle retail who bought Grayscale’s four-year cycle note. Price drifts, then cracks. The narrative of “2026 is the year” gets quietly repriced to “2027 maybe.”

Who holds the bag? ETF retail buyers who entered on the cycle thesis without a structural view. Late LTH sellers who waited too long and are now selling into a falling bid instead of a rising one. Miners who need price above their break-even to stay solvent.

I am not calling a cycle top. I am saying the structural evidence for a sustained move higher is thinner than the consensus assumes. The cohorts that should be leading the charge are net sellers. That matters more than a four-year pattern.

What I’d Actually Do With a Position Right Now

For the next four to six weeks, I would not be adding long exposure here on the cycle thesis alone. The macro floor — DXY weakness, marginal balance sheet expansion — justifies holding existing exposure without panic. It does not justify sizing up. The on-chain picture is telling me this is a rally that needs to prove itself, not one I want to front-run.

The USDC minting data is the one signal I’m watching most carefully. If that $253M in stablecoin creation over a 12-hour window reflects genuine buy-side staging — and we see it translate into spot inflows and improving ETF net flows over the next two weeks — I would revisit the thesis. Stablecoin minting that converts into Bitcoin spot demand is a real signal. Stablecoin minting that sits idle is just defensive positioning in dollar form.

The one metric that breaks this thesis: Weekly spot ETF net flows turning positive above $150M sustained for two consecutive weeks, paired with LTH supply change reversing from net distribution back to net accumulation. If both conditions are met simultaneously, the structural argument against the rally collapses and the macro tailwind becomes the leading story. I’d add exposure then.

Until that’s confirmed: the bid the consensus is counting on isn’t showing up in the data. And I’d rather be wrong and miss the first 10% than be right about the structure and wrong about the timing.